ARIMA

Learn how autoregression, differencing, and moving-average error terms combine into one unified model you can fit, diagnose, and forecast with.

What you'll learn

- AR(p), differencing d, and MA(q): what each parameter controls and why they are combined

- The Box-Jenkins workflow: stationarity check, ACF/PACF identification, fitting, residual diagnostics, forecasting

- How to use statsmodels ARIMA, interpret AIC/BIC, and verify that residuals look like white noise

Before you start

The last three lessons built the pieces separately: differencing to kill a trend, AR for the persistence of levels, MA for the reverberation of shocks. This lesson bolts all three into one model — the workhorse of univariate forecasting — and, just as importantly, the disciplined workflow for using it without fooling yourself.

What ARIMA is

ARIMA(p, d, q) stands for AutoRegressive Integrated Moving Average. The three letters encode a recipe:

- Difference the raw series

dtimes until it is stationary. - Fit an AR(p) + MA(q) model on that differenced series.

- Integrate back (reverse the differencing) to get forecasts in the original units.

The word “integrated” here is the inverse of differencing: if you difference once to remove a trend, you integrate once (cumulative sum) on the way back out.

The three parameters

| Symbol | Name | What it controls |

|---|---|---|

p | AR order | How many of the series’s own past values feed into today’s prediction |

d | Differencing degree | How many times to subtract consecutive values to achieve stationarity |

q | MA order | How many past forecast errors feed into today’s prediction |

An ARIMA(1, 1, 1) model says: difference the series once, then predict with yesterday’s differenced value plus yesterday’s error.

Stationarity and the role of d

A stationary series has a constant mean and variance over time. Trending or drifting series are not stationary, which breaks ordinary AR and MA fitting. Differencing once removes a linear trend; differencing twice removes a quadratic one. In practice d is almost always 0, 1, or 2. Choosing d too large is a common mistake — see the warning below.

The Box-Jenkins workflow

George Box and Gwilym Jenkins formalized a five-step loop that remains the standard approach for fitting ARIMA models:

Step 1 — Make the series stationary (choose d).

Plot the series. If it trends, compute the first difference. Run an Augmented Dickey-Fuller (ADF) test or KPSS test. Repeat until the test indicates stationarity.

Step 2 — Identify p and q from ACF and PACF.

- The autocorrelation function (ACF) measures correlation between the series and its own lags. An MA(q) model cuts off after lag

q. - The partial autocorrelation function (PACF) removes the influence of intermediate lags. An AR(p) model cuts off after lag

p. - In practice the patterns overlap, so treat ACF/PACF as a starting point, not a rule.

Step 3 — Fit the model.

Pass (p, d, q) to your fitting routine and estimate the parameters by maximum likelihood.

Step 4 — Diagnose residuals. This is the step most beginners skip — and the most important. If your model has captured all signal, the residuals should look like white noise: zero mean, constant variance, no autocorrelation. Check:

- A residual ACF plot: no spikes outside the confidence band.

- The Ljung-Box test: a significant p-value means autocorrelation is still present and your model is underfit.

Step 5 — Forecast.

Call .forecast(steps=h) for an h-step-ahead forecast. Uncertainty widens with horizon.

Model selection: AIC and BIC

When comparing candidate orders, use the Akaike Information Criterion (AIC) or Bayesian Information Criterion (BIC). Both penalize models for complexity. Lower is better. BIC applies a heavier penalty for extra parameters, so it tends to favor sparser models.

A practical shortcut is pmdarima.auto_arima, which searches over a grid of (p, d, q) values, runs stationarity tests automatically, and returns the order with the lowest AIC. It is a useful starting point, but always inspect the residuals of whatever it returns.

The ARIMA pipeline — diagram

The ARIMA pipeline: difference → AR+MA fit → integrate back → forecast (widening band = growing uncertainty).

Fitting ARIMA in Python

The code below shows the full Box-Jenkins pipeline using statsmodels; run it locally in any Python environment with pip install statsmodels.

import pandas as pd

import matplotlib.pyplot as plt

from statsmodels.tsa.stattools import adfuller

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.tsa.arima.model import ARIMA

from statsmodels.stats.diagnostic import acorr_ljungbox

# --- Step 1: load and inspect ---

series = pd.read_csv("monthly_sales.csv", index_col="date", parse_dates=True)["sales"]

# ADF test for stationarity

adf_result = adfuller(series)

print(f"ADF p-value: {adf_result[1]:.4f}") # p < 0.05 => stationary

# First difference if needed

diff1 = series.diff().dropna()

adf_diff = adfuller(diff1)

print(f"ADF p-value (diff=1): {adf_diff[1]:.4f}")

# --- Step 2: ACF / PACF plots to choose p and q ---

fig, axes = plt.subplots(1, 2, figsize=(12, 4))

plot_acf(diff1, lags=20, ax=axes[0])

plot_pacf(diff1, lags=20, ax=axes[1])

plt.tight_layout()

plt.show()

# --- Step 3: fit ---

model = ARIMA(series, order=(2, 1, 1)) # p=2, d=1, q=1

result = model.fit()

print(result.summary()) # AIC, BIC, coefficient estimates

# --- Step 4: diagnose residuals ---

result.plot_diagnostics(figsize=(12, 8))

plt.show()

lb = acorr_ljungbox(result.resid, lags=[10], return_df=True)

print(lb) # p-value >> 0.05 => residuals look like white noise

# --- Step 5: forecast ---

forecast = result.forecast(steps=12)

print(forecast)

conf_int = result.get_forecast(steps=12).conf_int()

print(conf_int)To make it concrete, here is the fit-and-forecast core run on a synthetic trending series (an ARMA process plus a slow upward drift, so it genuinely needs d=1):

import numpy as np, pandas as pd

from statsmodels.tsa.arima.model import ARIMA

# Synthetic series with trend (built to need one difference)

np.random.seed(3)

s = build_synthetic_series() # 180 monthly points, trend + ARMA structure

result = ARIMA(s, order=(2, 1, 1)).fit()

print("AIC:", round(result.aic, 1))

fc = result.get_forecast(steps=18)

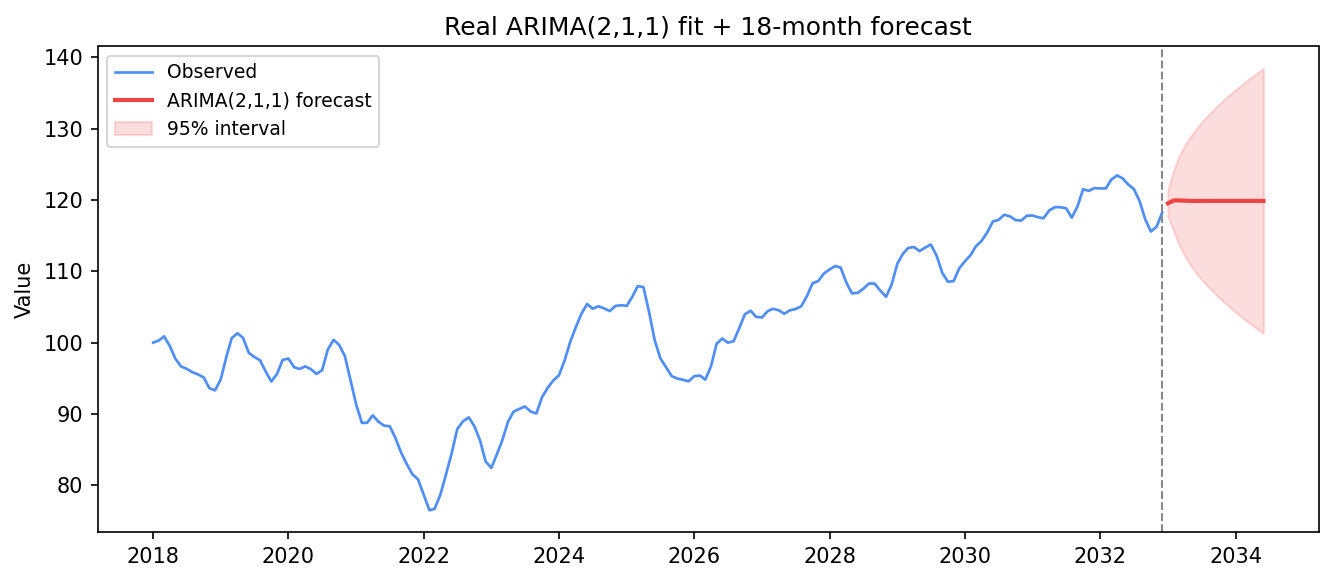

mean, ci = fc.predicted_mean, fc.conf_int() # point forecast + 95% bandAIC: 505.0

A genuine ARIMA(2,1,1) forecast: the red point forecast settles near the recent level while the 95% band fans out — uncertainty growing the further ahead you look.

Two things to read off that band. It widens with horizon — the model is honest that month 18 is far less certain than month 1. And the point forecast quickly flattens toward a level rather than continuing any short-term wiggle, because ARIMA reverts to the mean of the (differenced) process at long range. Never over-interpret a far-out point forecast; the band is the real message.

Reading .summary()

The summary table includes:

- coef — estimated AR and MA coefficients.

- P value — whether each coefficient is statistically significant.

- AIC / BIC — use these to compare competing orders; lower wins.

- Ljung-Box (Q) — the null is no autocorrelation; a large p-value here is what you want.

Auto-selection with pmdarima

from pmdarima import auto_arima

auto_model = auto_arima(

series,

seasonal=False,

information_criterion="aic",

stepwise=True,

trace=True,

)

print(auto_model.summary())auto_arima runs ADF tests internally, tries many (p, d, q) combinations, and returns the lowest-AIC model. Always verify the residuals even when using auto-selection.

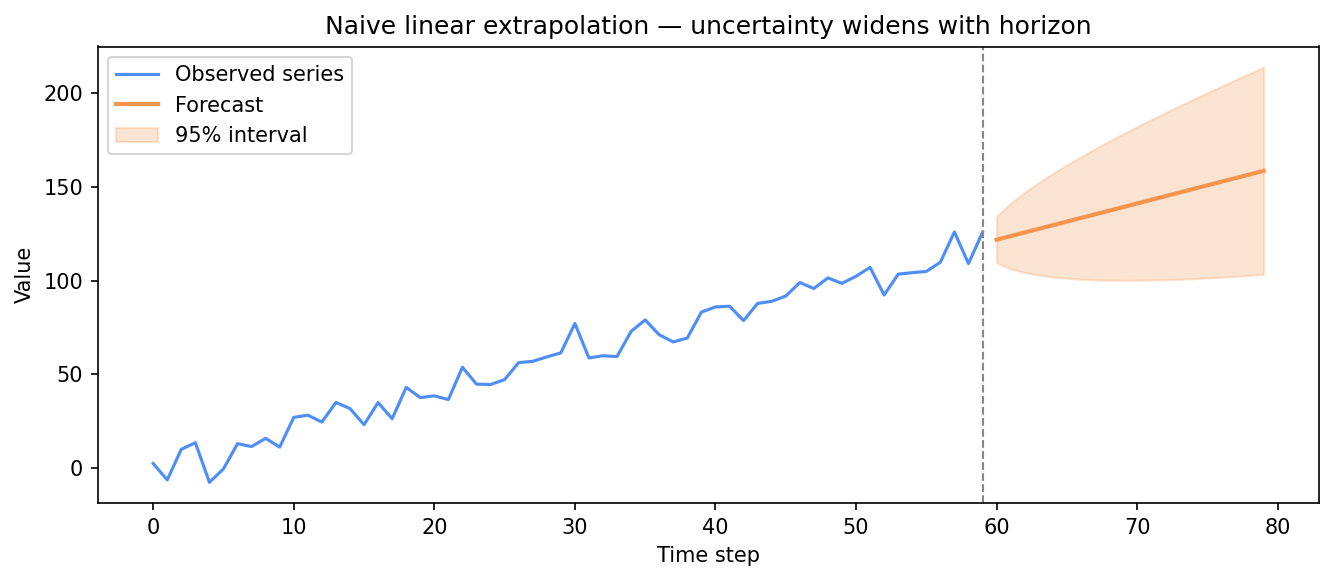

Seeing forecast extrapolation intuitively

The playground below uses only NumPy and Matplotlib. It fits a simple linear extrapolation on a synthetic trending series and plots the forecast as a naive intuition-builder — not a real ARIMA fit. The widening band represents how uncertainty grows with horizon.

import numpy as np

import matplotlib.pyplot as plt

rng = np.random.default_rng(42)

# Synthetic series: linear trend + noise

t = np.arange(60)

series = 2.0 * t + rng.normal(scale=8, size=60)

# Naive "forecast": extend the linear trend estimated from the last 30 points

fit_window = series[-30:]

x = np.arange(30)

slope, intercept = np.polyfit(x, fit_window, 1)

horizon = 20

h = np.arange(1, horizon + 1)

forecast = slope * (30 + h) + intercept

# Growing uncertainty band (simplification: grows as sqrt of horizon)

sigma = np.std(fit_window - (slope * x + intercept))

band = 1.96 * sigma * np.sqrt(h)

fig, ax = plt.subplots(figsize=(9, 4))

ax.plot(t, series, color="#4f8ef7", label="Observed series")

f_t = t[-1] + h

ax.plot(f_t, forecast, color="#f7954f", linewidth=2, label="Forecast")

ax.fill_between(f_t, forecast - band, forecast + band,

color="#f7954f", alpha=0.25, label="95% interval")

ax.axvline(t[-1], color="#888", linestyle="--", linewidth=1)

ax.set_title("Naive linear extrapolation — uncertainty widens with horizon")

ax.set_xlabel("Time step"); ax.set_ylabel("Value"); ax.legend()

plt.tight_layout()

plt.show()

print("Slope:", round(slope, 3), "| Intercept:", round(intercept, 3))Slope: 1.934 | Intercept: 61.867

A toy linear extrapolation (slope ≈ 1.93). The band is narrow at step 1 and fans out by step 20 — uncertainty grows with horizon, just like a real ARIMA forecast.

The recovered slope (≈ 1.93) sits close to the true 2.0, and the confidence band fans out as you go further into the future — exactly how a real ARIMA forecast behaves: the further out you forecast, the less certain the model is.

In one breath

ARIMA(p, d, q) = AutoRegressive Integrated Moving Average: difference the series d times to make

it stationary, fit AR(p) on past values and MA(q) on past errors, then integrate (cumulative-sum) the

forecasts back to the original scale. Fit it with the Box-Jenkins loop — stationarise → identify

p,q from ACF/PACF → fit by maximum likelihood → diagnose the residuals → forecast — and the step

beginners skip is the diagnosis: residuals must look like white noise (flat residual ACF, large Ljung-Box

p-value), because a good AIC with autocorrelated residuals is still a bad model. Use AIC/BIC (lower

wins) to rank candidate orders, auto_arima as a starting search, and remember forecasts revert to the

mean far out — read the widening band, not the point.

Practice

Quick check

A question to carry forward

Look at where ARIMA quietly fails — the last practice question is the tell. Fit a clean ARIMA to daily data and a stubborn spike reappears in the residual ACF at lag 7; on monthly data it returns at lag 12. That’s the diagnosis step doing its job: it’s flagging a pattern ARIMA structurally cannot capture. The December bump from the very first time-series lesson never went away — plain ARIMA just has no vocabulary for “every 12 steps.”

So the question to carry forward is: how do you give the model a way to learn a seasonal rhythm — a

correlation not with last month, but with the same month last year? The next lesson, SARIMA, adds a

second, seasonal (P, D, Q) triple operating at the seasonal period, so the model can finally difference

“versus last December,” not just “versus last month” — and that lag-12 residual spike disappears.

Practice this in an interview

All questionsChoose d by differencing until the ADF test confirms stationarity; choose p from the PACF cutoff and q from the ACF cutoff on the differenced series; then confirm with AIC or BIC to guard against over-fitting. In practice, an automated grid search over a small range of candidates with information criteria is more reliable than visual inspection alone.

A Vector Autoregression (VAR) model extends ARIMA to multiple time series simultaneously: each variable is regressed on its own past values and the past values of all other variables in the system. Use VAR when the series have mutual predictive relationships (Granger-causality) and you want to model those interactions; ARIMA is sufficient when one series can be forecast in isolation.

ARIMA(p,d,q) models non-seasonal series by combining autoregression, differencing, and a moving average of errors. SARIMA extends it with a second set of seasonal parameters (P,D,Q,s) that operate at the seasonal lag s, handling periodic patterns that ARIMA alone cannot capture.

Prophet is a curve-fitting model that decomposes the series into trend, seasonality, and holidays; it handles missing data, multiple seasonalities, and non-uniform time grids with minimal tuning and is accessible to non-statisticians. ARIMA is a statistical model based on autocorrelation structure; it is more appropriate when the series is short, noise is small, and you need principled uncertainty intervals from an explicit stochastic process.